It may be prepared in one of two ways, using either the indirect or the direct method. Although information presented in the operating activities section is different, both methods yield the same cash flows from operating activities amount. The indirect method is more popular because the information needed to prepare the section is readily available on the income statement and balance sheet. The choice of methods pertains only to the operating activities section. The investing and financing section both are prepared using a direct method. Note how Wellbourn’s ending cash balance of $135,500, from the statement of cash flows for the year ended December 31, matches the ending cash balance in the balance sheet on that date.

What is the purpose of a cash flow statement?

Cash inflows are listed first and each begins with “Cash received from…” Cash outflows follow and each begins with “Cash paid for…” If there is more than one inflow, they are subtotaled in the middle column. If a fixed asset’s balance increases from one year to the next, it means that more must have been purchased and there was a cash outflow. Similarly, if a fixed asset’s balance decreases from one year to the next, it means that some or all of it was sold and there was a cash inflow. To help determine the amount of cash received or paid, refer to the journal entry for each transaction to see if Cash was debited or credited. The statement of cash flows is based on information from the income statement, retained earnings statement, and balance sheet.

Summary of Investing and Financing Transactions on the Cash Flow Statement

My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. The non-cash expenses and losses must be added back in and the gains must be subtracted. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own. Thus, when a company issues a bond to the public, the company receives cash financing.

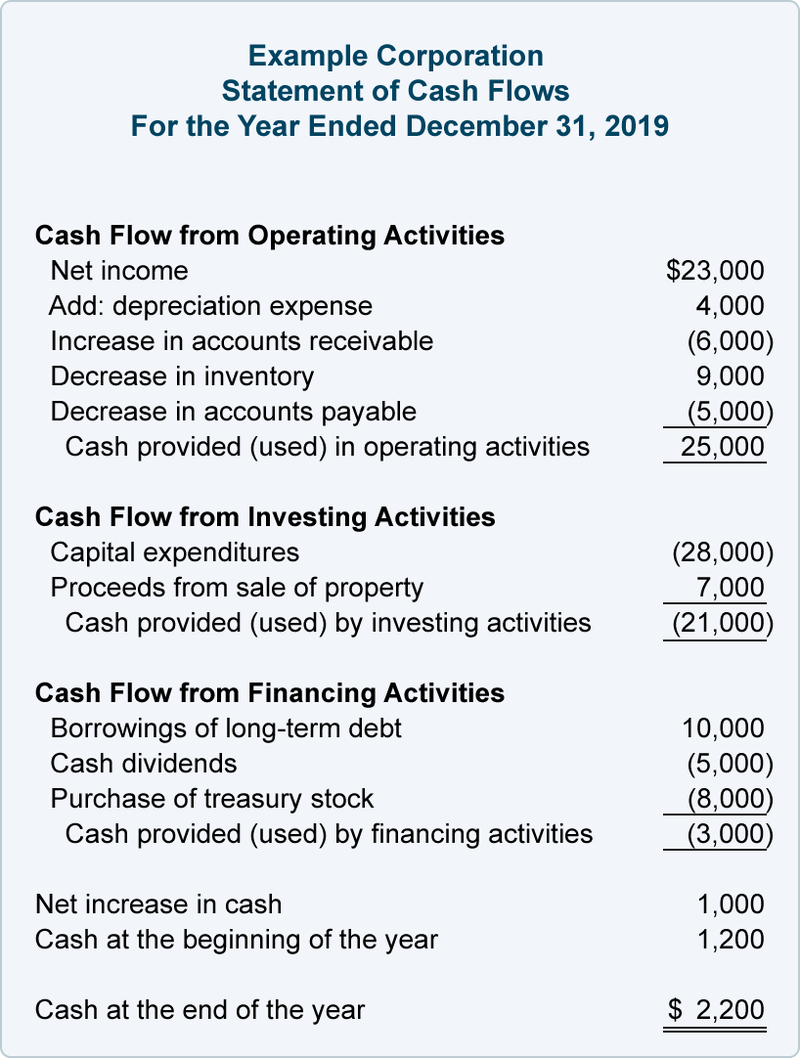

Example of the Statement of Cash Flows Indirect Method

Free cash flow is the available cash after subtracting capital expenditures. This information allows businesses to forecast future cash needs, make informed investment decisions, and track actual performance against budgeted targets. Management can use the information in the statement to decide when to invest or pay off debts because it shows how much cash is available at any given time. As a result, the business has a total of $126,475 in net cash flow at the end of the year. Transactions in CFF typically involve debt, equity, dividends, and stock repurchases.

Ask a Financial Professional Any Question

If the starting point profit is above interest and tax in the income statement, then interest and tax cash flows will need to be deducted if they are to be treated as operating cash flows. Clearly, the exact starting point for the reconciliation will determine the exact adjustments made to get down to an operating cash flow number. Assume that you are the chief financial officer of a company that provides accounting services to small businesses. Further assume that there were no investing or financing transactions, and no depreciation expense for 2018. Conversely, if a current liability, like accounts payable, increases this is considered a cash inflow. This is because the company has yet to pay cash for something it purchased on credit.

- Negative cash flow typically shows that more cash is leaving the company than coming in, which can be a reason for concern as the company may not be able to meet its financial obligations in the future.

- Common activities that must be reported as investing activities are purchases of land, equipment, stocks, and bonds, while financing activities normally relate to the company’s funding sources, namely, creditors and investors.

- This is the final piece of the puzzle when linking the three financial statements.

- Let’s take a closer look at what cash flow statements do for your business, and why they’re so important.

This section records the cash flow between the company, its shareholders, investors, and creditors. Analysts look in this section to see if there are any changes in capital expenditures (CapEx). It can be considered as a cash version of the net income of a company since it starts with the net income or loss, then adds or subtracts from that amount to produce a net cash flow figure. Let’s say we’re creating a cash flow statement for Greg’s Popsicle Stand for July 2019. For small businesses, Cash Flow from Investing Activities usually won’t make up the majority of cash flow for your company.

If you run a pizza shop, it’s the cash you spend on ingredients and labor, and the cash you earn from selling pies. If you’re a registered massage therapist, Operating Activities is where you see your earned cash from giving massages, and the cash you spend on rent and utilities. When your cash flow statement money basics: managing a checking account shows a negative number at the bottom, that means you lost cash during the accounting period—you have negative cash flow. It’s important to remember that long-term, negative cash flow isn’t always a bad thing. For example, early stage businesses need to track their burn rate as they try to become profitable.

The payable arises, or increases, when an expense is recorded but the balance due is not paid at that time. An increase in salaries payable therefore reflects the fact that salaries expenses on the income statement are greater than the cash outgo relating to that expense. This means that net cash flow from operating is greater than the reported net income, regarding this cost. There are too many transactions to make it practical to look at each one individually to determine its impact on cash flow. Therefore, the income statement and comparative balance sheet numbers will be used to efficiently remove non-cash transactions in order to arrive at the net cash flow from operating activities number. Operating activities are those involved in the day-to-day running of the business.

Using this method, cash flow is calculated through modifying the net income by adding or subtracting differences that result from non-cash transactions. This is done in order to come up with an accurate cash inflow or outflow. A cash flow statement (CFS) is a financial statement that captures how much cash is generated and utilized by a company or business in a specific time period. Purchase of Equipment is recorded as a new $5,000 asset on our income statement. It’s an asset, not cash—so, with ($5,000) on the cash flow statement, we deduct $5,000 from cash on hand. For most small businesses, Operating Activities will include most of your cash flow.

On the same day you pay your cell phone bill and car insurance payment for a total of $210. The net cash inflow on that day is $160; that is, $160 more came in than went out. Keep in mind that these formulas only work if accounts receivable is only used for credit sales and accounts payable is only used for credit account purchases.

Propensity Company sold land, which was carried on the balance sheet at a net book value of $10,000, representing the original purchase price of the land, in exchange for a cash payment of $14,800. The data set explained these net book value and cash proceeds facts for Propensity Company. Direct cash flow statements show the actual cash inflows and outflows from each operating, investing, and financing activity. While the indirect cash flow method makes adjustments on net income to account for accrual transactions. We sum up the three sections of the cash flow statement to find the net cash increase or decrease for the given time period. This amount is then added to the opening cash balance to derive the closing cash balance.